IIT Regulations Clarify the Tax Treatment for Expatriates in China

In October 2018, China’s Ministry of Finance proposed the draft changes to the Implementing Regulations of the IIT Law, to become effective by January 2019. In many ways these regulations are more important than the IIT Law itself (see our original article on the IIT law here: https://rplawyers.com/articles/changes-to-individual-income-tax-law-to-impact-companies-operating-in-china/), as it was the regulations that previously contained many of the special rules that applied to foreigners working in China, including the various special deductions for expatriates and the “Five-year tax rule”. The proposed draft regulations address the major concerns of the expatriate community. We summarize the key regulations below.

- China’s “Five-year tax rule” on Global Income to change to the “Six-year tax rule”

With the changes to residency rules in the new IIT Law, many China analysts mistakenly believed that the “Five-year tax rule” on exemption for declaration and taxation of non-China related global income would no longer exist. However, the rule was always defined in the implementing regulations rather than the IIT Law itself. The proposed draft implementing regulations changes the “Five-year tax rule” to the “Six-year tax rule”. In short, foreigners that have stayed in China for at least six years will become taxable on their global income, but this period can be reset by staying outside of China for 30 consecutive days.

- Exemption Mechanisms for Chinese and Expatriates

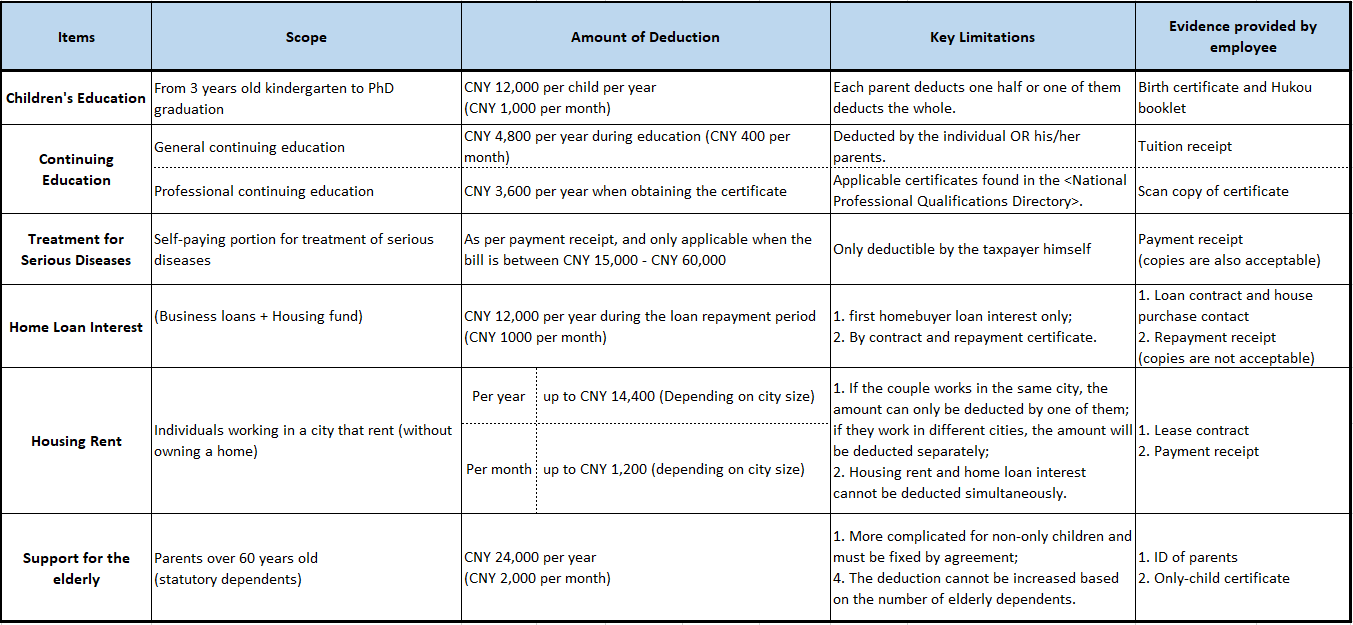

Under the previous implementing regulations, several categories of expenses could be exempted from individual income tax, though foreigners enjoyed the broadest scope of deductions. As the IIT law introduced a more limited set of exemptions for Chinese nationals, the concern was that this would apply to expatriates as well. The draft implementing regulations and related implementing policies have now clearly defined the deduction thresholds for Chinese individuals and required documentation, which R&P summarizes below:

R&P further notes that the thresholds for deductions will remain the same for at least all of 2019, and that any amount not deducted within the following calendar year shall not carry forward.

In principle, the above deductions apply to expatriates as well. However, the implementing regulations do not confirm how this will impact the already expansive expatriate tax free benefits. For now, the original 1994 regulations on tax deductible items for expatriates will continue to be effective. This means that deductible items and mechanisms will for the most part remain unchanged for expats, while expats may be able to enjoy some additional deductions such as for support of the elderly or treatment for serious illnesses.

3. Global Income Reporting for High net-worth individuals

Notwithstanding the above, one of the clear objectives of the new IIT Law is to combat tax base erosion and tax evasion by strengthening global income reporting procedures and eliminating the possibility of using offshore affiliated entities and bank accounts to lower individuals’ tax burdens. Article 8 of the revised IIT Law added many new considerations that the authorities will use to combat tax evasion.

The implementing regulations of the IIT law introduce the global reporting mechanism and a system of foreign tax credits, as well as the thresholds for controlled and affiliated entities, and the definition of “low tax regions” (i.e. 12.5% or lower for general corporate income tax). The tax authorities will become more aggressive in pursuing cases where they believe the individual is evading taxes, and therefore high net-worth individuals should review the voluntary reporting and tax credit quota systems. With the standard definitions and thresholds now in place, individuals and companies operating in China will be better able to assess their tax risks under the new IIT Law.

4. Closing Remarks

The Implementing Regulations of the IIT Law have assuaged many of the fears with the new law that most concerned expatriates. The “Five-year tax rule” has changed to the “Six-year tax rule”, and the expatriate deductions will remain (for now); while lower tax rates and expanded deductions will benefit all those working in China. Now the last challenge remains: employers must ready themselves for significant changes to reporting and administrative burden come January 2019.